06 Apr. 2024

My Thoughts on CreditCorp’s Business Focus

Roger McKay

TGIF! Ping!!

My first thought: How come, it’s Friday! My cell should be on ‘do not disturb’. Let me check notifications. Consumer credit launched!

‘Vibing to when the gbedu dey enter body’

Skimming through and thinking out loud, with Twitter as the medium, so many questions fueled by excitement and whiskey.

Visiting the website, it says, ‘Income is just the start of purchasing power.’ In my head, finally!!!! The start of a credit economy in my Angel chosen country, Nigeria. Ugh! Inflation. But that’s not why I’m here.

So this morning, I read through the business focus again, and I can’t contain my excitement. What I see and can feel, and that’s why I am putting it into words by breaking the business focus down for you.

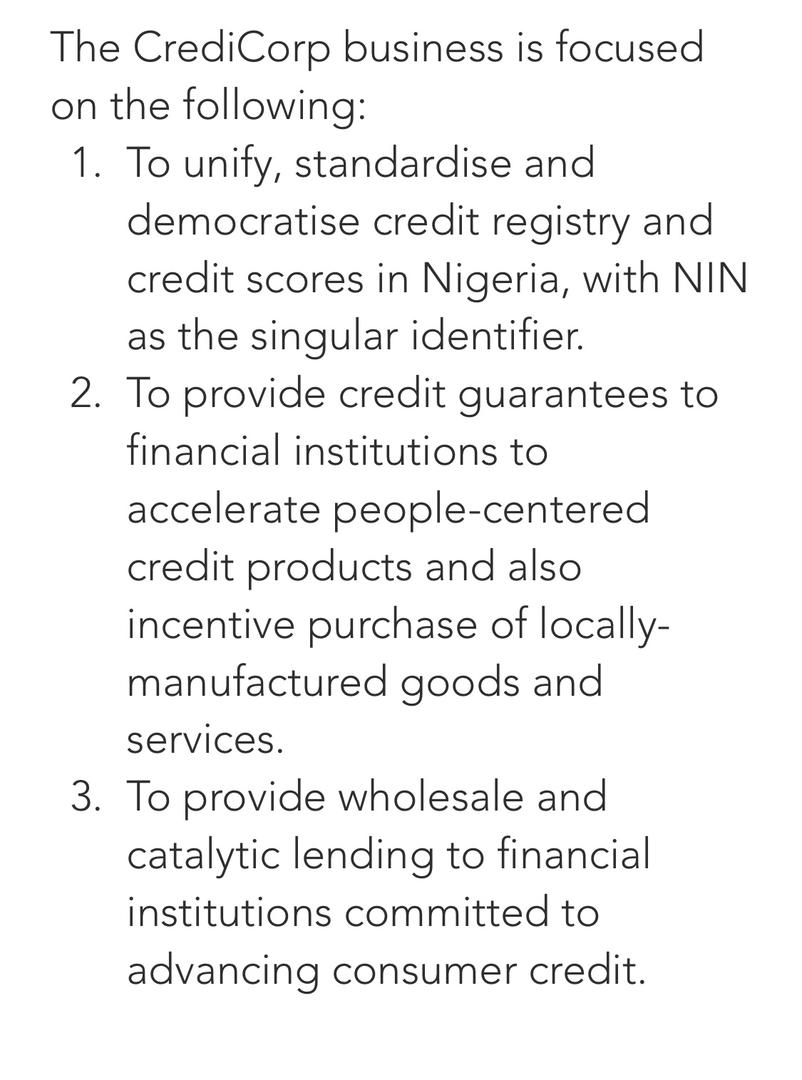

Business Focus 2.

As you know, I am a big advocate of a pure credit money economy and there’s nothing stopping Nigeria from being one. Now, with an effective implementation of mandate 2, it can catalyze things at a much faster pace than we imagine.

Whoever wrote this has an incredible insight. So, to make it clear, CreditCorp on business focus 2 is tasked with:

1. Providing credit guarantees

2. Enabling the creation of people-centered credit products

3. Incentivizing the purchase of locally manufactured goods and services.”

So, credit guarantee is basically a tool used to mitigate risk. It’s like Credit Corp saying, ‘Roger, please lend Tinubs $50. I promise you, if Tinubs doesn’t pay back his $50, I’d give you another $50.’ What happens is, this makes me feel safe lending Tinubs money,

Now, because of this guarantee, I become more innovative. Instead of always focusing on payday loans, I can start creating and distributing great and impactful credit products in respect to the Nigerian market like device financing, auto loans, HELOCs, store credit, etc., with great loan characteristics depending on the product created.

And you know what the first and second order effects are, guys? Businesses can then increase their revenue through credit-led sales. (At least I can start a subscription-based business 🤣) Production increases, jobs are created, businesses can expand their operations, unemployment is reduced, income levels increase, consumption rises, and the economy is stimulated. It’s like killing thirty birds with one stone fa! (That’s how Ilorin people express importance)

Business Focus 1

Ummm, you guys know I have always had concerns about our bureaus, identification, credit scoring, and the education regarding all of this. Well, I don’t know their plans, but two words struck out, as I have always advocated:

1. Standardizing

2. Democratizing”

So, Nigeria has about four Credit Reference Organizations, and basically what these guys do is collect and maintain credit information. If CreditCorp is thinking about standardizing, I believe it would involve the reference agencies being more transparent about the process, methodologies, and factors in which those credit scores are calculated. This includes collection and reporting.

I mean, very important standards are maintained, some lenders do not send information to the bureau. Plus, as for the data sharing by those lenders, I share the sentiments of the bureau being too expensive for a startup, so the need to rely on third-party API providers who only provide but don’t give you access to report information on the obligor.

And I also think the registry should be opened up; let’s get alternative data from landlords, supermarkets, telcos, small businesses, etc. And most importantly, education. To be honest, some of my guys don’t know that the credit registry gives them access to a free credit score report once a year.

With NIN being a single identifier, it’s going to be a game changer, considering the type of data that would be linked with our NIN.

When this happens, there would be a comprehensive profile of individuals, thus enhancing accuracy in credit assessment and inclusivity in the ecosystem. I look forward to the implementation.

Business Focus 3

So, wholesale lending is basically saying, instead of CreditCorp starting to lend out to every Romeo & Juliet, it can say, ‘Roger, I’d give you $500 so you can lend to at least 30 Romeo & Juliet,

While catalytic lending is like saying, ‘Roger, I am giving you $1000 so that every Romeo who wants to lend for the purpose of getting a car can have one.’

If this is done right, one thing is certain: credit will be very affordable

But I have questions that need to be answered:

1. How would it be funded?

2. What is the loan origination process, and who handles it?

3. Who underwrites it?

4. I learned there’s a bank guarantee for every BOI loan; would it be similar?

5. What’s the process of partnership?

6. Would the credit product be revolving, installment, or both?

7. Should banks be worried?

8. If it would be distributed by banks and fintechs, how do they earn? Would earnings be capped?

9. The interest rate: would it be on par with the inflation level?

10. What measures would be put in place to prevent fraud and abuse?

11. How would the effects of the initiatives be monitored, and would the reports be available to the public?

12. How would capital be allocated amidst partnering institutions

13. What criteria would be used to determine capital allocation among partnering institutions

14. Will there be opportunities for smaller or newer institutions to participate in partnerships

Overall, I'm rooting for CreditCorp's success and wisdom for its management. Their mission has the power to change countless Nigerian lives for the better. It's a real game changer, and I'm proud to witness it happening in my lifetime.